Inflation has conditioned American consumers to flinch at prices that once seemed reasonable. Groceries, fuel, utilities and even digital subscriptions all feel like they’re on a slow, relentless upward arc. Watching money leave your account with each swipe without a clear payoff feels like willingly letting cash slip into a void.

The feeling is psychological as well as economic. Many have instinctively begun to ask: “If I must spend, why not get something back?”. That instinct is exactly why cashback credit cards have become one of the most sought-after financial perks in the United States. Now, consumers can earn a slice of their own spending back — in the form of statement credits, direct deposits or even digital rewards. Read more on CredHelper.

Why cashback cards became America’s favorite perk

These days, credit cards are loyalty programs designed to encourage behavior rather than being used to accumulate debt.

The best cashback programs exist because card issuers compete hard for your attention, and they’re willing to trade a small percentage of every purchase back to you to win it.

Multiple financial analysts, including institutions like the American Bankers Association, note that rewards cards continue to grow in popularity as consumers become savvier about personal finance and demand transparency and return on spending.

Unlike travel points that might require blackout dates or airline partnerships, cashback is straightforward: you spend, you get a fraction of that back.

Because of its simplicity, even those who aren’t fixated on spreadsheets and reward multipliers can understand the idea.

Many top offers include cash rebates on groceries, gas, dining and recurring bills, cementing cashback as a mainstream benefit for everyday transactions rather than a niche travel perk.

In 2025, the shift toward consumer-centric reward systems is more pronounced than ever, especially among younger adults who prioritize flexibility over traditional banking loyalty.

Credit card cashback: check top rewards tailored for you

Not all cashback cards are created equal. The secret is to get the right kind of rewards, not just any rewards. Some cards offer flat rates on all purchases; others provide tiered bonus categories.

A thorough comparison uses current offerings to identify which cards align with your spending pattern. Here’s what card seekers typically evaluate:

- Flat cashback cards that return the same percentage on every purchase, ideal for broad spending habits;

- Tiered rewards cards with enhanced percentages on specific categories like supermarkets, gas or dining;

- Rotating category cards that switch seasonal or quarterly bonus categories;

- Introductory offers that include bonus cash back after meeting a minimum spend.

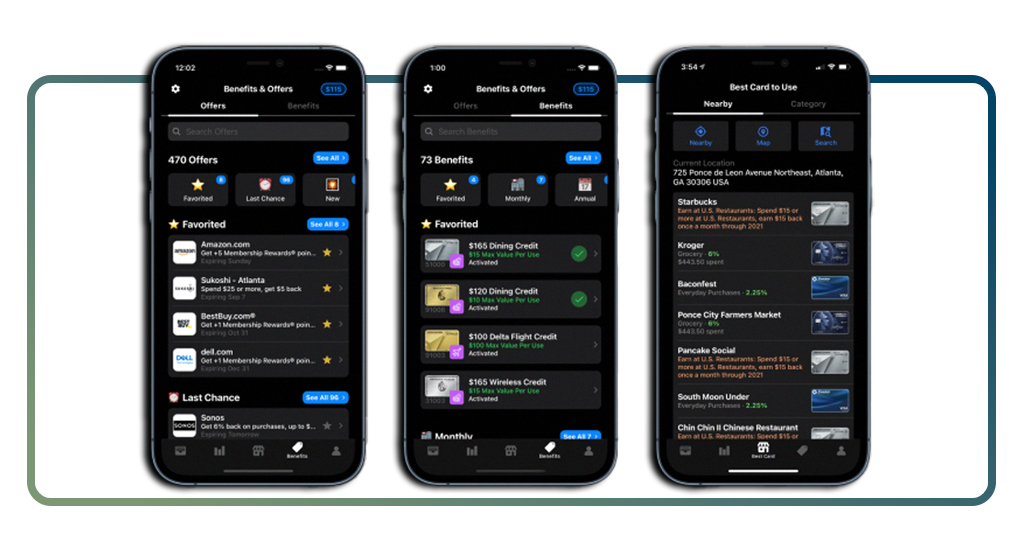

Tools like Max Rewards (also available for Android and iOS) compile these options in one place, allowing you to compare side-by-side by reward rate, welcome bonus and annual fee structures.

You also can browse cards, filtering by category and see current promotions at a glance. With an overview of your own expenses — groceries, fuel, utilities, restaurants, streaming — you can match a card whose bonus structure reflects where you spend.

Discover cards with bonus categories you already use

Some card issuers reward purchases differently. For example, a card might offer elevated cashback on gas stations and groceries because those categories represent consistent, repeat spending for most households.

Others might feature higher returns for dining and entertainment, which benefits frequent travelers and social spenders. A checkpoint for maximizing your 2025 cashback potential is identifying which of these apply:

- Categories that represent your monthly essentials;

- Strategic spending bursts you know you’ll hit (like a big grocery run or annual subscriptions);

- Seasonal patterns like holiday shopping or travel bookings;

- Opportunities to earn elevated rewards via merchant partnerships or promotional categories.

The math behind this is simple: directing everyday expenses through a card that offers a higher rebate, even by a few percentage points, multiplies into real returns over 12 months.

A calculator online or an app like Max Rewards can help estimate annual cashback potential based on your typical monthly spending habits.

Calculate your annual cashback potential

Understanding your future rewards begins with a simple exercise: list your major spending categories and estimate monthly totals. Then, match those with the reward rates provided by the card you are considering.

For example, if you spend most of your monthly budget on groceries and your card returns enhanced cash back for that category, your year-end rebate can be significantly higher than a card with a flat rate.

You can do this calculation manually, but referral calculators and comparison tools on Max Rewards automatically perform this analysis once you input your estimated spending ranges.

This transforms an abstract “I think I’ll make money back” into a clear projection: “I will get $X back this year”.

Understanding this potential also helps you see which cards make sense relative to annual fees.

In many cases, a card with no fee and a modest rebate can outperform a pricey premium option with a high rate but minimal bonus categories for your lifestyle.

How to apply online and get approved faster

Once you identify the card that aligns with your spending profile, applying becomes the next step. Digital applications have streamlined what used to be a paperwork gauntlet into a 10-minute process.

Want to increase your chances of approval? Check this:

- Review your credit score beforehand using a free service or a score app;

- Ensure your reported income and employment status are accurate and current;

- Check for prequalification options on comparison tools like Max Rewards before submitting hard inquiries;

- Avoid applying for multiple cards in a short timeframe to prevent unnecessary dips in your credit profile;

- Fill out the application with consistent data matching your financial history.

Max Rewards often includes links that direct you to issuer application pages once you select a card, simplifying the process from comparison to completion.

Final thoughts: protect your financial edge with cashback

Consumers in 2025 face a dual reality: costs rising steadily while personal budgets remain flat. A well-structured cashback strategy is one of the most tangible ways to reclaim value from routine spending.

When you start optimizing credit card choices based on where you spend most; groceries, fuel, dining, subscriptions; the sense that “money just leaves” begins to feel outdated. Instead, spending becomes an activity with potential upside.

That shift is emotional as much as economic: you feel smarter, less passive, and more in command of daily finances. Check top offers, compare bonus categories you already use, and apply for a card that matches how you live.

Protect your financial edge, make the rewards work for you, and turn everyday purchases into ongoing, automatic savings.