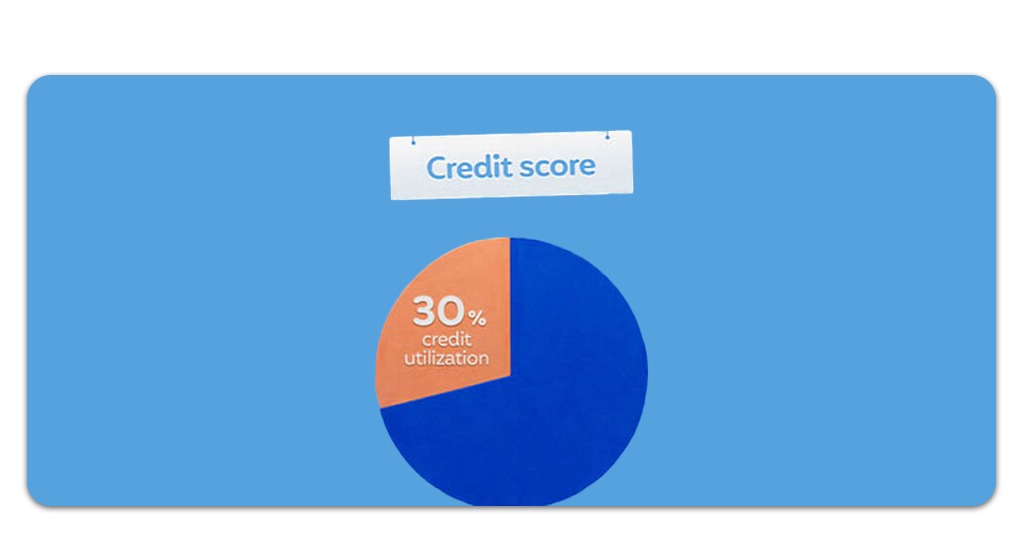

Credit utilization below 30% represents one of the most misunderstood aspects of personal credit, even though it influences approval decisions and long-term financial flexibility. Usually, people assume that paying bills on time tells the full story, but credit reports evaluate how available credit is managed month after month. This disconnect leads to frustration when credit limits appear generous but scores remain sensitive to small changes. Understanding how utilization operates reframes credit cards from spending tools into strategic instruments that reflect financial discipline.

Maintaining credit utilization below 30% brings predictability into a system that feels opaque. And, with that, borrowers gain control over how lenders interpret their behavior in real time. This perspective changes attention from minimum payments to balance management, where timing and proportional use carry measurable consequences. CredHelper will show you that once this logic becomes clear, credit decisions feel less reactive, making every charge and payment contributes to a visible ratio.

The FICO Score Impact: Why Credit Utilization Below 30% Matters

Credit utilization below 30% plays a decisive role in how creditworthiness is interpreted across scoring models.

Even with consistent payment history, high utilization signals dependency on borrowed funds, which lenders interpret as elevated risk.

This metric reflects how much of the available credit is actively used at any moment. Lower ratios suggest restraint and planning, while higher ratios imply financial pressure despite on-time payments.

Small changes in balances can produce noticeable score movement. Utilization updates frequently, explaining why scores react faster to balance shifts than to long-term behaviors.

Keeping this ratio controlled stabilizes the credit profile, and predictability becomes a visible pattern.

Understanding the Weight of Utilization in Your Credit Profile

Utilization influences scoring more heavily than many expect, shaping how lenders interpret day-to-day credit behavior beyond simple repayment discipline.

Its position just behind payment history gives it substantial practical relevance, especially during evaluations tied to approvals and interest conditions.

Also, higher limits paired with restrained balances suggest financial breathing room, while cards operating near their ceiling signal reduced flexibility.

Moreover, a single account carrying a high balance can outweigh the positive effect of several cards that remain lightly used.

Balanced usage patterns communicate control and predictability, forming a unified financial signal rather than isolated behaviors.

The Calculation: How Your Ratio Is Determined

When you keep your credit below 30%, it relies on a straightforward ratio, although its effects extend far beyond the simplicity of the formula.

That’s because the reported balance is measured against the total available credit across accounts, determining how lenders assess proportional usage rather than absolute spending.

Balances reflected on credit reports originate from statement dates instead of payment due dates. This timing difference explains why scores sometimes change even when payments feel punctual and responsible.

Both overall utilization and individual card ratios influence the profile at the same time, increasing sensitivity to isolated balance shifts.

Understanding this reporting cycle brings coherence to score movement, and updates often occur before most people recognize that a new balance has already been recorded.

What Happens When You Exceed the Critical Threshold

When credit utilization rises above the 30% mark, lender risk perception is ringed immediately, since even modest balance increases begin to suggest tighter financial margins and reduced short-term flexibility.

As utilization climbs, lenders interpret the reduced available credit as a weaker buffer against income variation or unexpected expenses.

Repeated movement above this threshold reinforces a behavioral pattern rather than an isolated fluctuation, and scoring models respond more strongly to recurring signals than to single-cycle anomalies.

Although recovery remains fully achievable, restoring confidence depends on maintaining lower balances consistently across several reporting cycles rather than relying on one-time adjustments.

Actionable Secret: Timing Your Payments

Payment timing plays a decisive role in determining which balances appear on credit reports because credit bureaus record amounts based on reporting cycles.

Despite cardholders assuming that due dates govern reporting behavior, statement closing dates define the balances lenders actually see, creating score changes that often feel unexpected.

Aligning payments with reporting cycles allows utilization to decrease without altering spending behavior.

This awareness introduces leverage into credit management, making away from surprise score movements and toward deliberate anticipation of how balances are displayed.

Paying Balances Before the Statement Date vs. Due Date

Then, paying balances before the statement date lowers the amount reported to credit bureaus, influences directly in the utilization ratios and improves score stability during each cycle.

On the other hand, paying only before the due date avoids interest charges, although reported balances may still appear elevated and continue to affect utilization metrics.

Separating these two timelines clarifies outcomes, and interest management and credit scoring respond to different triggers within the billing process.

Combining early balance reduction with on-time final payments produces greater consistency, reinforcing both financial efficiency and score resilience.

Strategies for Maintaining Low Utilization

When you keep credit utilization below 30%, it remains sustainable when supported by structural habits, with smaller and more frequent payments preventing balances from accumulating unnoticed.

Also, distributing spending across multiple cards reduces concentration risk, helping individual card ratios remain balanced even during higher spending periods.

Periodic credit limit increases support utilization passively, as higher available credit lowers ratios without requiring behavioral change.

Budget visibility reinforces consistency, and platforms such as Mint assist balance tracking in a centralized way that reduces manual oversight.

The Secret to Keeping Credit Utilization Below 30% – Conclusion

This is basically how keeping credit utilization below 30% reshapes how credit activity is interpreted. Understanding this ratio simplifies why scores fluctuate and how small adjustments produce meaningful results.

Managing utilization introduces intention into credit use. And topics like timing, balance awareness, and structural habits replace guesswork with control.

This perspective does not require financial advice. It relies on visibility and consistency applied over time. When utilization remains predictable, credit profiles communicate reliability long before applications occur.

Related: Dominate Your Finances with this Budgeting App

Looking for financial tips? Favorite CredHelper to learn how to manage your finances like a pro using the best available tools.